Most fashion fans think Prada vs Miu Miu bags come from completely different supply chains. The brands look different. Their prices are different. So it feels natural to assume everything behind them is separate.

But the reality is more complex.

Both brands belong to Prada Group. They share parts of their procurement networks, factories, and digital systems. However, the way each brand manages its bag supply chain creates different market results.

From Italian leather sourcing to global distribution, small strategic differences shape how their bags perform. These details reveal how luxury bag supply chains work inside a large fashion group.

Prada and Miu Miu: One Supply Chain Serves Both Brands

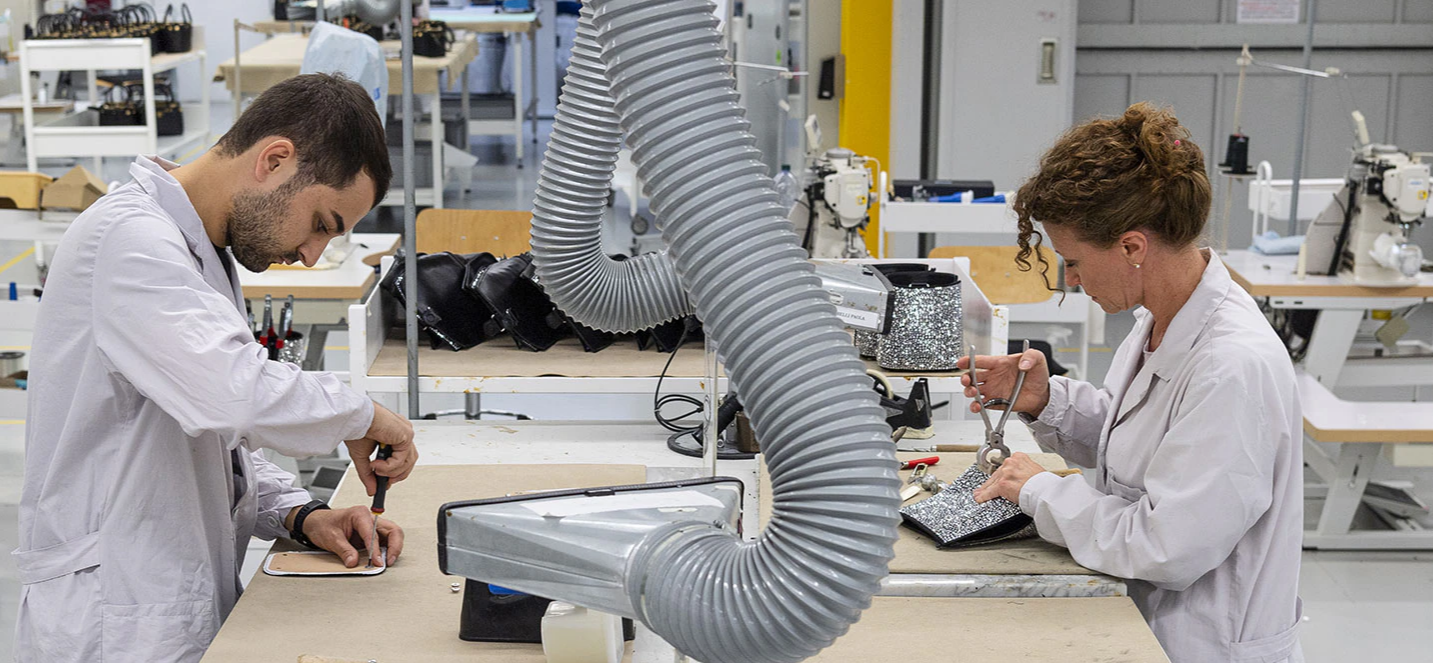

Prada Group runs one central supply chain. This chain serves five brands: Prada, Miu Miu, Church’s, Car Shoe, and Marchesi. Many assume sister brands use separate bag factories and bag suppliers. This system proves otherwise.

Both brands share the same infrastructure:

-

25 production sites across key Italian regions—23 facilities in Tuscany and Umbria make leather goods, knitwear, handbags, accessories, and footwear for Prada and Miu Miu

-

€300M+ total investment (2019-2025) builds capacity and preserves craft skills. It also drives vertical integration. €60M goes to 2025 alone

-

10% equity stake in Rino Mastrotto Group locks in leather and textile supplies for all brands

-

o9 Solutions AI partnership gives real-time buying insights and risk checks. The system is optimized for leather goods production across both labels

New sites opened in Piancastagnaio, Gubbio, Northampton, and Foiano della Chiana. These expansions support production for both brands.

The group cut 222 suppliers between 2020-2025. This came from 850+ audits. Over 25% of inspections led to fixes or termination. No unauthorized outsourcing is allowed. This protects quality for Prada and Miu Miu at the same time.

Shared Procurement Networks: How Both Brands Source Materials

Prada Group uses a centralized buying system that follows top industry practices. This structure strengthens its luxury leather bag supply chain across both brands. The group owns a 10% stake in Rino Mastrotto Group, securing premium leather and textile supplies for Prada and Miu Miu. Instead of relying on standard supplier contracts, the group builds equity partnerships to lock in long-term material stability.

Companies that develop deep supplier partnerships capture 63% more value than those using traditional buyer–seller relationships. Teams using digital procurement tools can also improve efficiency significantly through integrated sourcing platforms.

Real-Time Material Intelligence Across Brands

The o9 Solutions AI partnership drives shared material sourcing decisions. The platform provides real-time data on leather availability and textile pricing, while also tracking supply risks. This level of visibility is critical for luxury bag production planning, where timing and material consistency directly affect delivery schedules.

Global procurement platforms like this are expanding quickly. The market is expected to reach USD 12.9 billion by 2033, growing at a 13.7% CAGR. These systems allow Prada Group to coordinate suppliers efficiently across all its brands.

Both Prada and Miu Miu benefit from the group’s supplier streamlining strategy. Between 2020 and 2025, the group reduced its supplier base by 222 vendors. This reflects a broader trend, as 82% of companies are narrowing vendor lists to improve pricing power and reduce operational complexity. To maintain standards, the group conducts more than 850 audits, with 25% of inspections resulting in corrective actions or contract terminations.

Shared Sustainability Commitments

Material sourcing now reflects stronger sustainability goals. Around 71% of procurement programs focus on environmental standards, up 13 percentage points since 2021. Prada Group builds joint leather partnerships that support sustainable leather bag sourcing, including low-carbon materials and circular production programs. Both Prada and Miu Miu benefit from these shared initiatives.

This network also gives the group buying power that neither brand could achieve alone. Volume discounts, early access to supplier innovation, and diversified risk exposure are major advantages. Today, 63% of companies rely on geographic diversification and multi-sourcing strategies to strengthen supply chain resilience.

Production Technology: Group-Wide Digital Transformation

Prada Group applies digital technology across every production line serving both Prada and Miu Miu. AI-driven predictive systems and real-time IoT sensors operate in all 25 facilities. This infrastructure strengthens luxury bag manufacturing efficiency by reducing downtime and aligning production schedules between the two brands.

Advanced AI and machine learning platforms predict equipment failures before they happen. Sensors collect data from knitting machines, leather cutting tables, and stitching stations. The system can identify maintenance needs days in advance, reducing unplanned downtime by up to 40%. As a result, both labels maintain stable output while improving overall equipment utilization.

Digital Twins Simulate Production Without Disruption

Digital twin technology creates virtual models of production lines. Teams test new bag designs or demand spikes in advance. This improves luxury bag production scalability, allowing Prada and Miu Miu to shift capacity without stopping real production.

Edge computing processes sensor data directly on the factory floor. Systems adjust stitching tension and leather cutting depth in real time, ensuring consistent quality for high-end bags.

The o9 Solutions platform also forecasts production needs and runs supply chain simulations. This helps Prada Group prepare for delays or demand changes.

To support this shift, the group has committed over €300M to smart factory upgrades, aligning with the global rise in automation and IoT adoption.

Bag Distribution Strategy Differences: The Real Divergence

Prada and Miu Miu share bag factories, procurement networks, and production technology. But their distribution strategies show the sharpest split. The group gives each brand distinct market positioning. They do this through store placement, inventory timing, and regional rollout priorities.

Store Network Design: Positioning Through Placement

Prada runs 618 owned stores (DOS) worldwide as of 2024. These stores anchor luxury shopping districts in major cities. Miu Miu operates fewer standalone boutiques. It targets high-traffic, trend-driven locations. The brand picks neighborhoods with younger shoppers and fashion-forward retail.

Both brands avoid placing stores near each other. You’ll seldom see Prada and Miu Miu on the same street. This geographic separation stops customer overlap. It strengthens brand identity differences. Cities like Milan, Paris, and Tokyo have multiple Prada locations. These serve established luxury buyers. Miu Miu boutiques sit near modern fashion retailers and lifestyle spots.

Inventory Flow Timing: Staggered Market Releases

Distribution timing follows different seasonal calendars. Production runs through shared facilities, yet release schedules differ. Miu Miu ships new collections to stores 2-3 weeks earlier than Prada seasonal drops. The brand captures trend-setters and social media buzz before main luxury season peaks.

Prada releases align with traditional luxury buying cycles. Pre-fall and resort collections hit stores at specific times. High-net-worth clients refresh wardrobes during these periods. This staggered approach maximizes shelf time for both brands. No internal competition happens.

Regional allocation patterns differ too. Miu Miu focuses on Asian markets—China, Japan, and South Korea in particular. Younger luxury buyers show strongest growth there. The brand saw 89% revenue growth in recent periods. These markets drove most of that growth. Prada maintains balanced global distribution. It emphasizes European heritage markets and established Middle Eastern clientele.

Digital Channel Strategy: Platform Separation

E-commerce platforms run separate storefronts. Backend integration exists, but Prada.com and MiuMiu.com offer distinct experiences. You get different visual merchandising and customer communication styles. This digital separation extends the brand positioning from physical retail.

The distribution split proves something clear. Shared chains don’t need unified go-to-market strategies. Prada vs Miu Miu shows how luxury groups use distribution as the main tool for brand differentiation. Production infrastructure stays consolidated throughout.

Regional Bag Market Execution: Same Infrastructure, Different Priorities

Prada and Miu Miu use the same 25 production facilities and unified procurement networks. But their regional market strategies show very different commercial priorities. Both brands deploy shared infrastructure through distinct geographic execution models. These models mirror broader luxury retail patterns across key markets.

Asia-Pacific: Miu Miu’s Growth Engine

APAC markets generate 40% of Miu Miu’s revenue expansion. This far outpaces Prada’s regional performance. The brand focuses inventory allocation and marketing spend in China, South Korea, and Japan. These markets show the strongest appetite for trend-driven luxury among younger demographics.

Miu Miu releases products in these territories 2-3 weeks earlier than European releases. This timing captures social media momentum before Western markets see them. K-pop collaborations and localized digital campaigns perform best here. The brand now runs dedicated flagship concepts in Seoul and Shanghai. These showcase seasonal collections through Instagram-optimized retail experiences.

Prada maintains balanced geographic distribution across APAC. But it prioritizes heritage positioning. Store placements favor established luxury shopping districts. Inventory flows follow traditional seasonal calendars. No accelerated drops.

North America and Europe: Strategic Separation

Both brands serve Western markets through 618 combined owned stores. But placement strategies differ. Prada anchors prestige locations—Fifth Avenue, Bond Street, Avenue Montaigne. These stores target high-net-worth clientele seeking timeless luxury.

Miu Miu selects trend-forward retail zones. These sit near contemporary fashion retailers and lifestyle destinations. SoHo, Le Marais, and Milan’s Corso Como district host boutiques designed for younger luxury shoppers. This geographic separation prevents customer overlap. It also maintains distinct brand territories.

European markets see staggered inventory releases between brands. Prada aligns with Paris Fashion Week cycles and traditional pre-fall/resort buying periods. Miu Miu ships collections earlier to capture trend-setter attention. This happens before main luxury season peaks.

Emerging Markets: Infrastructure vs. Execution

The brands share distribution center capacity and logistics networks across Latin America, the Middle East, and emerging Asian markets. But execution priorities differ based on market maturity, shaping their luxury bag distribution strategy.

Miu Miu tests new markets through pop-up stores and department store concessions before opening standalone boutiques. This matches its agile bag strategy: enter fast, measure demand, then scale successful products.

Prada, by contrast, launches full-scale flagship stores in cities like Dubai, São Paulo, and Mumbai. These moves reflect long-term investment in established luxury markets.

This shows that differentiation between Prada and Miu Miu happens through market prioritization, not separate infrastructure. Both operate within the shared logistics system of Prada Group, but apply different go-to-market approaches for their bags.

Conclusion

The Prada vs Miu Miu supply chain comparison shows an interesting contrast. Both brands use nearly the same infrastructure. Yet they see very different growth rates. They share procurement networks, production facilities, and digital projects under Prada Group’s central management. But Miu Miu’s 58% revenue jump proves something key. Supply chain efficiency is just half the story. Strategic positioning matters more.

The real difference isn’t how products are made. It’s what gets made and where it’s sold. Miu Miu targets younger buyers. The brand offers accessible luxury prices. Plus, it expands aggressively into Asia-Pacific markets. This shows how brand strategy can make the most of shared operations.

Fashion industry professionals and luxury retail investors can learn from this. Supply chain integration builds the foundation. Brand-specific execution drives success. Both labels are investing €400 million in supply chain expansion through 2026. Watch how Prada Group balances shared operations while keeping each brand distinct.

Need deeper insights into luxury fashion bag supply chains? Check out our analyses of LVMH’s multi-brand operations. We also cover Kering’s vertical integration strategies.